First announced in February 2023, the Division 296 tax on higher superannuation balances has now passed Parliament and will be effective from 1 July 2026.

The legislation has had many changes in the 3 years since it was first announced, some positive and others more problematic. Outlined below are the details of how Division 296 tax applies, what you need to know depending on age and circumstances and what actions you need to take today and into the future to minimise the likelihood of the tax causing you major issues.

The 3-step approach

In determining whether Division 296 tax applies to you, and if so, how much, there are three broad steps to consider.

Click the drop-down arrow to explore more for each step.

Step 1: are you above the relevant thresholds?

One of the key changes to the original draft legislation is the introduction of two different thresholds – a ‘large’ threshold and a ‘very large’ threshold – each of which is subject to increasing tax rates.

What are the thresholds?

The Division 296 tax applies a two-tiered approach:

| Large superannuation balance threshold – a 15% tax will apply to earnings attributable to the proportion of an individual’s superannuation balance that exceeds the ‘large superannuation balance threshold’ currently set at $3 million. |

| Very large superannuation balance threshold – a further 10% tax will apply to earnings related to the proportion of the individual’s superannuation balance that exceeds the ‘very large superannuation balance threshold’ currently set at $10 million. |

Both the large and very large superannuation balance thresholds will be indexed, ensuring they keep pace with inflation.

If you’re below the $3 million threshold, you won’t have to pay any Division 296 tax at this point in time – however as we highlight below, as your superannuation balance continues to grow and accumulate, you may be exposed to the tax in the future.

When are the thresholds applied?

Determining whether Division 296 tax applies from 1 July 2026 is now more straightforward: if your total superannuation balance exceeds the relevant threshold at either the beginning or end of the financial year, you will be subject to the tax.

There are however a couple of exceptions to highlight:

- Transitional year approach – for the first year that Division 296 tax applies, your total superannuation balance is only assessed at 30 June 2027 (in other words, the opening balance will be disregarded). In subsequent years, the assessment would use the higher of the beginning or ending balance for each financial year.

- Year of an individual’s death – the total superannuation balance is deemed to be nil at the end of the financial year of an individual’s death. This means that the default balance used for Division 296 tax purposes will be 1 July in the year of passing, resulting in a potential tax liability managed by the deceased’s estate.

Specific exclusions apply to the total superannuation balance such as structured settlements, child pensions and special rules for defined benefit funds. Capital Gains Tax (CGT) adjustments are available in certain circumstances – such as those for larger superannuation funds, members who are in pension phase or where a self-managed superannuation fund (SMSF) makes a CGT uplift election, something we look at later in this article.

Step 2: determine your earnings

Once you have concluded that you exceed the $3 million threshold, the next step is to calculate your ‘taxable superannuation earnings’. Broadly, this starts with each superannuation fund of which you are a member calculating your portion of Division 296 fund earnings (relevant superannuation earnings) and reporting this to the ATO – the aggregated amount collected by the ATO is known as your ‘total superannuation earnings’.

Earnings calculation and reporting requirements

Division 296 tax will apply to actual earnings and excludes unrealised capital gains. This is an important change from early announcements regarding Division 296.

Division 296 fund earnings is calculated by each superannuation fund of which you are a member using the following formula:

|

Each of these elements are defined – but in summary:

- Relevant taxable income or loss – this starts with taxable income and may be subject to certain adjustments.As an example, when a superannuation account is in Retirement Phase, certain capital gains that would normally be disregarded are adjusted and added back in this calculation. If you are a member of an Self Managed Super Fund (SMSF), an important once-off choice may be made in the context of unrealised capital gains (as discussed further below).

- Assessable contributions – this includes concessional contributions, such as superannuation guarantee payments.

- Net exempt current pension income – this relates to income not ordinarily subject to tax in the superannuation fund as it supports Retirement Phase interests.

- Non arm’s length component – this relates to non-arm’s length amounts received by a superannuation fund that are already taxed at the highest marginal tax rate.

- Pooled superannuation trust component – only relevant where a superannuation fund invests in units of a pooled superannuation trust.

The superannuation fund is expected to apply a ‘fair and reasonable’ approach to determine the proportion of Division 296 fund earnings that is attributable to your superannuation balance, which is then reported to the ATO. If you have multiple superannuation funds, these amounts will be aggregated by the ATO to determine your total superannuation earnings on which Division 296 tax is calculated. Actuarial certification may be required to determine this apportionment in particular circumstances, based on yet to be released regulations.

Once-off CGT election for SMSFs

A welcome transitional measure is the introduction of a once-off CGT election for a SMSF for Division 296 purposes only. Impacted SMSF members may request the SMSF trustee to make an irrevocable election to adjust the value (cost base) of all directly held assets in the SMSF to market value at 30 June 2026 for Division 296 purposes. The CGT election only affects Division 296 tax calculations for the individual (there will be no changes to the existing taxation of earnings in the superannuation fund – i.e. the cost base of the asset is only adjusted for Division 296 purposes, not for calculating tax on the regular earnings or gains of the fund).

This cost base adjustment will impact future CGT calculations attributable to the individual’s total superannuation earnings, subject to Division 296 tax.

Special transitional CGT adjustment provisions apply for other superannuation funds (non-SMSFs).

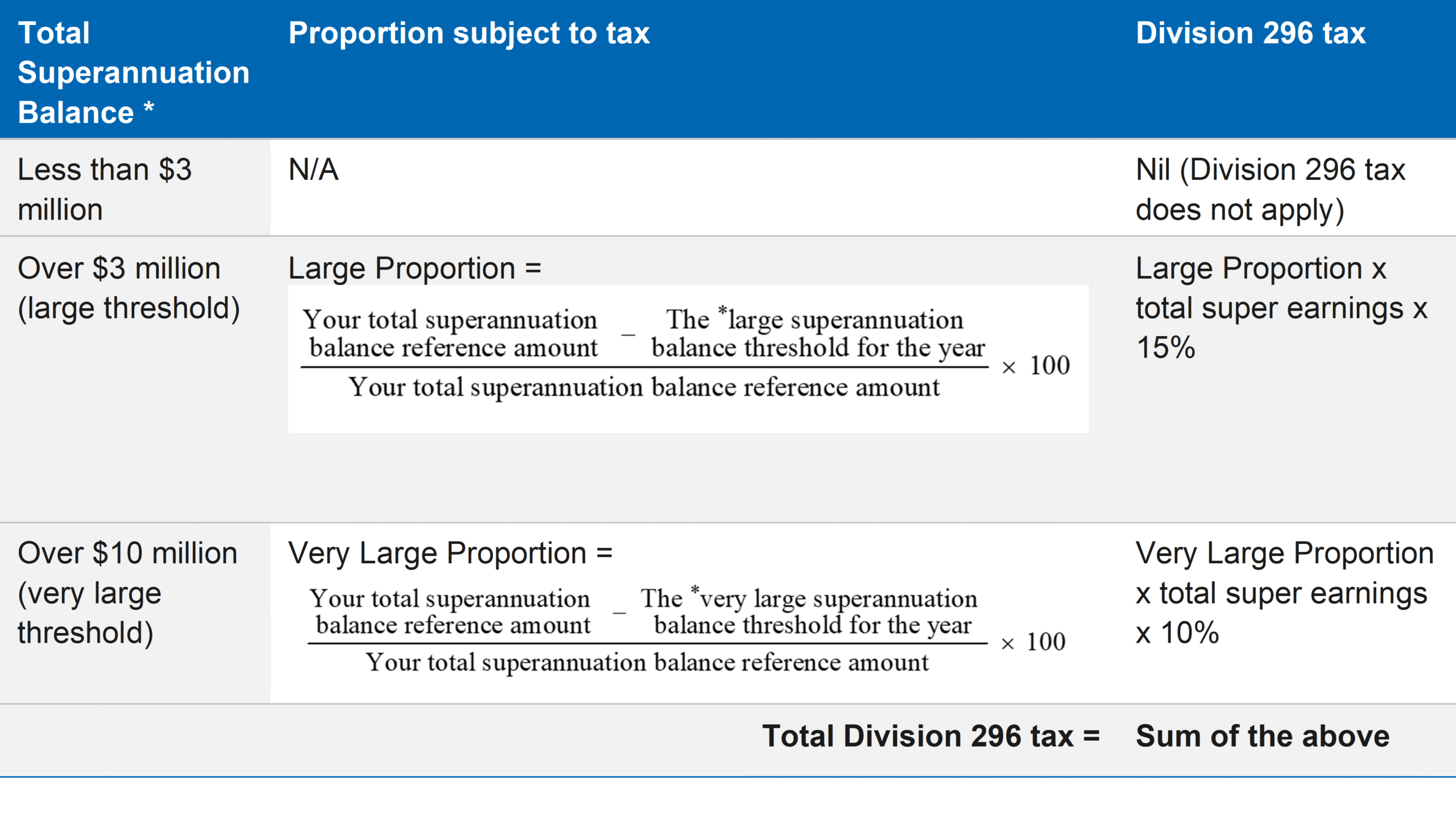

Step 3: calculate the Division 296 Tax

The rate of Division 296 tax is applied on the proportion of earnings that relate to a member’s total superannuation balance above the respective large or very large superannuation thresholds.

The table below illustrates how the Division 296 tax will apply based on the size of a member’s total superannuation balance. Importantly, earnings within the superannuation fund continue to be subject to ordinary tax rates of between nil and 15%, depending on personal circumstances (whether in Accumulation and/or Retirement Phase).

*Total Superannuation Balance is the higher of balance at the start or end of the financial year, except for the transitional year ending 30 June 2027 and year of death.

These calculations are illustrated in the following examples adapted from Treasury’s explanatory material.

| Example 1 | ||

|

|

Jordan has a Total Superannuation Balance of $4 million on 30 June 2027. As Jordan’s total superannuation balance exceeds the large superannuation balance threshold of $3 million in the first year (2026-27), Division 296 tax provisions will apply. | |

|

|

In the 2026-27 financial year, Jordan had total superannuation earnings of $100,000. | |

|

|

The proportion of his $4 million balance above the $3 million threshold is 25%. The proportion above $10 million is nil. | |

|

|

Jordan’s Division 296 tax liability is therefore $3,750 (being 15% x 25% x $100,000). | |

| Example 2 | ||

|

|

Kelly has a Total Superannuation Balance of $12 million on 30 June 2027 and $11 million on 30 June 2028. Division 296 tax only utilises the higher of these two balances, being the $12 million. | |

|

|

In the 2027-28 financial year, Kelly had total superannuation earnings of $500,000. | |

|

|

The proportion of her balance above the $3 million threshold is 75% and the proportion of her balance above the $10 million threshold is 16.67%. | |

|

|

Kelly’s Division 296 tax liability is therefore $64,585 (being [15% x 75% x $500,000] + [an extra 10% x 16.67% x $500,000]). | |

Who will pay the tax?

The Division 296 tax can be paid either personally by the individual or released from superannuation where a valid election is made.

The Division 296 tax will be due 84 days from the date the assessment is issued by the ATO.

What should you do now?

Those impacted by Division 296 tax should consider the potential ramifications that extend beyond superannuation – including cash flow, structuring and estate planning to name a few. The new tax also alters how superannuation data will be collected and reported to the ATO, impacting superannuation funds and related software providers.

Particular care should be taken with any changes that involve large withdrawals from superannuation – for example there are many legislative barriers that prevent individuals with pre-existing large superannuation balances from recontributing back into the superannuation environment.

Click to explore the below key areas that impacted individuals (or those who are nearing the threshold) should consider both now and into the future.

Review and identify opportunities in the transitional year ending 30 June 2027

- Determine if there are any opportunities to manage the Division 296 tax, such as cash flow considerations, asset valuations and whether a CGT uplift election should be made if in an SMSF. Undertake calculations to project and quantify the potential ongoing impost for impacted individuals.

Review your overall structure

- With the introduction of a higher effective tax rate of up to 40% for very large superannuation balances and up to a 30% effective tax rate for individuals with balances above $3 million, review of your existing structures to hold your wealth is more important than ever. Seek specialist advice on your overall investment structures and consider which investments are most tax-effective within different entities such as superannuation, companies or discretionary family trusts. These alternative structures may offer greater flexibility in managing tax outcomes and distributing wealth.

Age considerations

The impact of the Division 296 tax may have a materially different outcome based on your age and proximity to retirement:

- Members who are nearing or are in retirement have the opportunity to consider strategies such as managing drawdowns to potentially influence their total superannuation balance before 30 June 2027, alongside careful review of their superannuation investment strategy.

- Younger members will need to closely monitor their superannuation balances if they already have (or anticipate having) substantial amounts accumulated. This requires careful modelling and consideration of long-term asset allocations, as the introduction of the tax may create future cash flow implications and significant ongoing tax imposts.

Estate planning implications

- The legislation has changed the death tax outcomes where an individual holds more than the large superannuation balance threshold of $3 million in the year of passing. Consider how superannuation strategies such as reversionary pensions impact the beneficiary. As always, care should be taken before any changes are made in response to tax or legislative updates and how they could impact your estate and succession plans. Regular review and monitoring are key to ensuring your arrangements remain aligned with your estate planning objectives.

Asset protection

- While you may maximise tax effectiveness using particular structures, it’s important to balance this with protecting assets (whether in superannuation or alternative entities).

Valuation requirements

The evidence supporting superannuation asset valuations are likely to come under increased scrutiny:

- for the financial year ending 30 June 2026 for SMSF trustees that choose to make the CGT uplift election; and

- for the year ending 30 June 2027 onwards, particularly for SMSF trustees, as this will impact the total superannuation balance reported (and whether an individual is in or out of Division 296 tax territory).

While the Division 296 tax no longer applies to unrealised gains, the individual’s total superannuation balance remains impacted by the total value of superannuation assets, that is, it would include unrealised gains or losses on your assets, measured at the start and end of each financial year. Consider the administrative implications and potential costs associated with obtaining suitable valuation evidence to meet these ongoing requirements, weighing them against the benefits of the investment choices.

Asset types

- Is it optimal to house certain types of assets within superannuation or could alternative structures be more effective? Any review must be holistic, weighing not just superannuation or tax but also your broader financial circumstances.

- The nature of your assets and level of liquidity within superannuation requires careful planning. Holding illiquid or ‘lumpy’ assets could pose challenges if an impacted individual needs to fund the tax from cash reserves within superannuation.

The Division 296 tax applies from 1 July 2026, so the time for impacted individuals to act is now. To discuss how the changes may impact you, contact your local William Buck advisor.