We had thought mortgage holders might enjoy a brief reprieve around St Patrick’s Day, but we also cautioned that markets were underpricing the risk of a March hike, assigning probabilities closer to 10% at the end of February, well below our assessment of 40-45%. This was before the conflict in the Middle East began.

Today, after remarks from the RBA Deputy Governor the market probability jumped to 70% for a rate hike next week and combined with the impact from geopolitics, we now see a real possibility that a rate hike materialises next week.

The RBA has typically preferred to wait for quarterly inflation data with the next print due after the March meeting on 25 March, which is why the market reacted so strongly to Hauser’s comments. He appeared to be sending markets a warning shot. Indeed, he stressed “we have a problem with inflation” and inflation is “too high”. Further, he suggested the Middle East shock represents an upside risk to the Bank’s inflation projections.

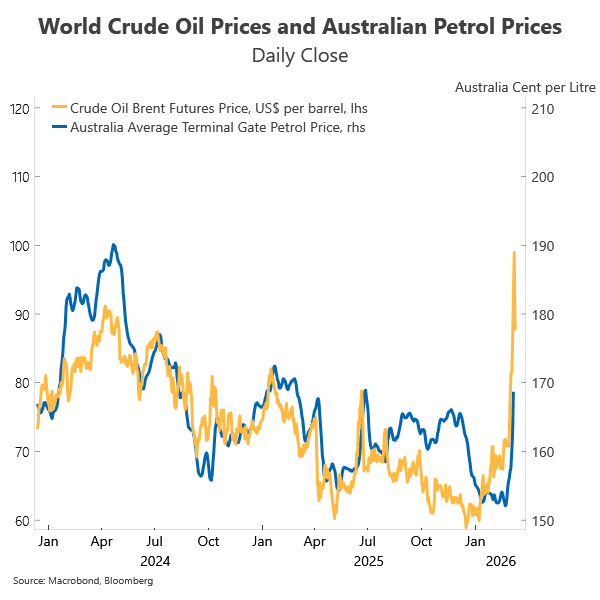

The duration and depth of the conflict are critical to the inflation outlook and remain highly uncertain. The disruption is not confined to a single channel. Energy is the most immediate and primary channel but not the only one. The price of Brent, a benchmark, rose to US$119.50 a barrel on Monday and is now trading at around US$87 a barrel. If it stays at this price, motorists can expect to pay another 20 cents at the petrol bowser.

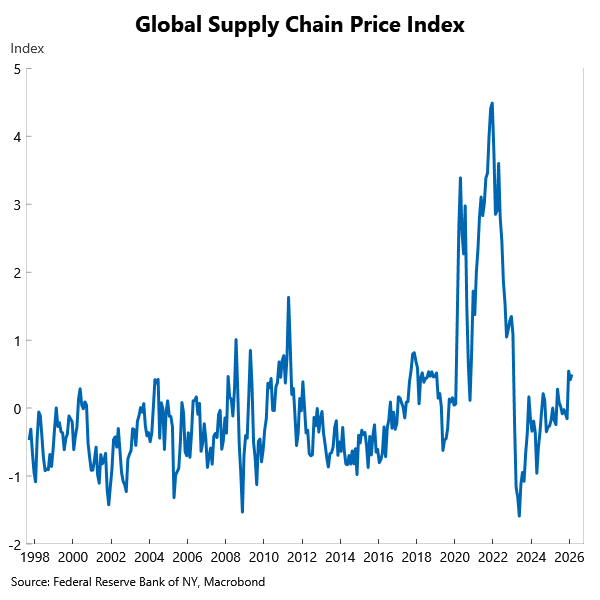

The Strait of Hormuz is effectively closed and 20% of crude oil moves through it. Refineries and facilities in Iran and in other Middle-Eastern countries are also impacted. Moreover, a third of the world’s fertiliser trade (urea, ammonia, phosphates) moves through this strait, which has implications for food prices. Supply disruptions extend beyond these two channels. Indeed, a widely-watched measure of supply-chain disruptions has risen to its highest since early 2023.

Central banks typically look through temporary price shocks and the uncertainty around its duration could give the RBA a reason to hold until May. But the longer the conflict persists, the greater the risk these supply‑chain pressures become entrenched and inflation expectations lift. This is the risk the RBA will be keen to head off and possibly sooner rather than later. Notably, the RBA’s most recent forecasts, published only last month, do not show inflation returning to the 2–3% target band until mid 2027, even before factoring in Middle-East developments.

One of the other key policy challenges for the Board is the tension between inflation risks and longer‑term growth headwinds. Ultimately, the RBA faces a clear trade‑off. Higher petrol prices and inflation will slow consumption and activity, but the Bank will focus on inflation first. Allowing inflation to remain elevated or rise further risks unanchoring expectations, a lesson central banks know well.

We see the March decision as a close call, but now favour a bring‑forward of the next hike to March given:

- stronger‑than‑expected GDP,

- renewed strength in job advertisements,

- persistently low unemployment, and

- rising upside risks to inflation and the higher inflation starting point

Our updated estimates are that underlying inflation is likely to print around 1.0% in the March quarter, lifting the annual rate to 3.6% in the year. That is up from 3.3% in Q4 and, with the quarter still unfolding, could prove higher.