Australian M&A market

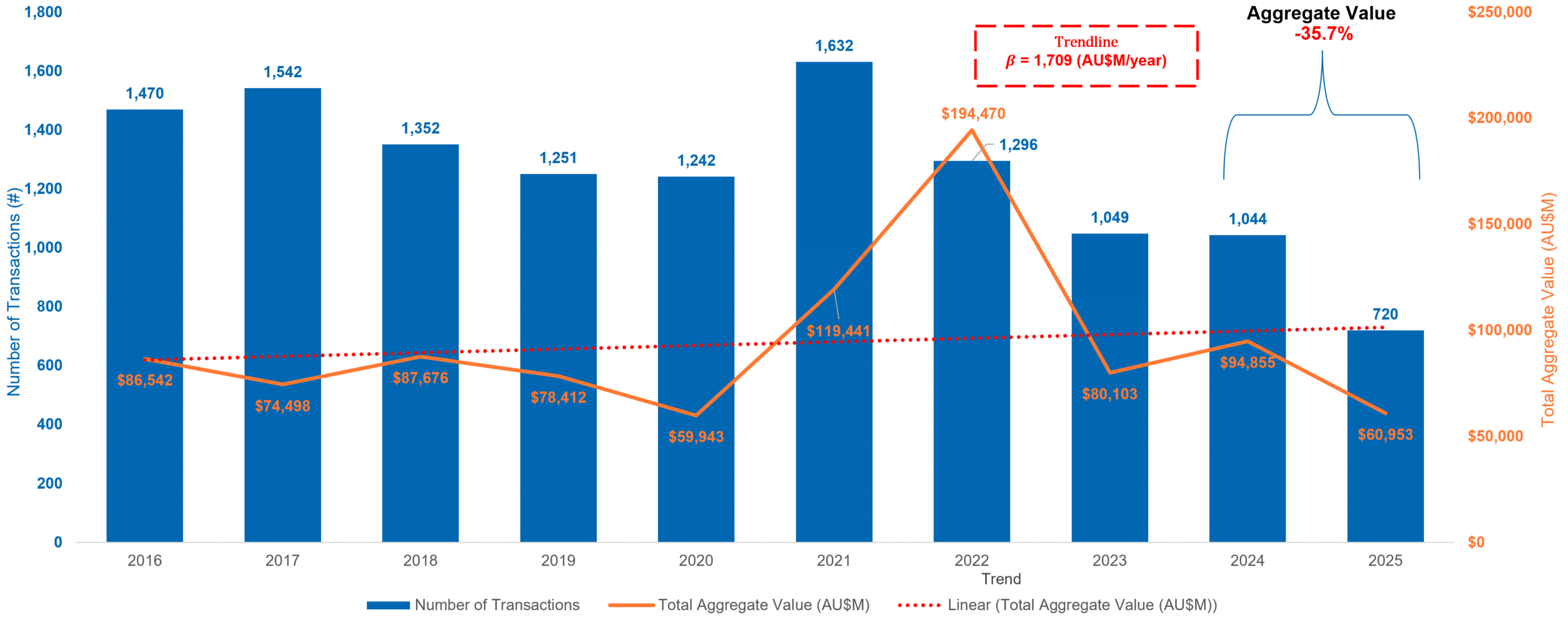

M&A activity in Australia reached a ten-year low in 2025 with just 720 completed deals and aggregate transaction value of $61 billion.

Looking back, activity is down from 1,044 deals in 2024, when total transaction value approached $95 billion and is a fraction of the 2022 peak when 1,296 transactions were completed with a combined value of close to $200 billion.

While this confirms the market is currently in a downturn from a deal activity perspective, the long-term trend for mid-market transactions remains positive.

Importantly, regulatory change accelerated dealmaking late in 2025 as buyers and sellers moved to complete transactions ahead of the ACCC’s (Australian Competition and Consumer Commission) new mandatory notification regimes which were introduced as of 1st January 2026.

The market has shifted decisively away from speculative growth and toward high-quality, defensible assets, particularly in:

- Materials sector (specifically critical minerals, copper)

- Industrials sector (cash-flow resilience to withstand economic uncertainty)

- Information Technology sector (selective, strategic assets)

Number and Aggregate Value of transactions in Australia (2016-2025)

Global vs Australian M&A

Undeterred by economic and geopolitical uncertainty, 2025 saw a significant rebound in M&A deal values globally.

According to the Bain & Co 2025 M&A reporti, deal activity globally rebounded sharply in 2025, with the value of M&A deals surging 40% to $US4.9 trillion, up from $US3.5 trillion in 2024.

This uplift was driven chiefly by technology and AI-related transactions, including Alphabet’s $US32 billion acquisition of Wiz and Palo Alto Networks’ $US25 billion purchase of CyberArk.

2025 also saw several sizeable minority investments, such as SoftBank’s $US40 billion commitment to OpenAI, and Meta’s $US14.3 billion investment in Scale AI, further underscoring the scale of capital flowing into AI-centric assets.

More broadly, the number of global deals increased by just 7%. This highlights that the surge in activity was led by a handful of megadeals rather than reflecting a broad-based expansion of transactions.

Australia’s market did not participate in this M&A rebound, reflecting its sector composition and limited exposure to global tech consolidation.

Samantha Nicholls

Partner, Corporate Finance

Tips from our experts

— If a sale is on the horizon, seek advice early to reduce risk and maximise value at transaction

— If growth and consolidation is your strategy, take advantage of businesses that have been ‘holding on’ for the last few years and strike when you can secure favourable deals quickly

— If your pathway isn’t fixed, avoid locking into one direction and be open minded and flexible for growth, capital raising or exit

Deal size and structure

Sub-$50 million transactions continue to dominate the Australian M&A market by volume (74%), underscoring the importance of smaller strategic acquisitions as bolt-on opportunities, vehicles for expanding market share, acquiring new technology or provide access to specialised talent.

Over the last decade, the number of $250m+ transactions has increased, reflecting periodic megadeal activity despite overall volatility. Examples of this are Northern Star’s acquisiion of De Grey Mining Limited for $5.6b and Vocus Group acquiring TPG Fibre network for $5.25b.

Private equity and strategic buyers are increasingly using partial acquisitions, earn-outs and public-to-private structures to bridge valuation gaps.

These structures allow buyers to manage risk and valuation uncertainty, while giving founders the opportunity to retain upside and stay involved.

Breakdown of M&A activity by transaction deal count per size in Australia (2016 – 2025)

Local vs foreign investment

In 2025, we saw foreign buyers represent nearly one in three (30%) of Australian transactions, the highest share in a decade. In fact, foreign participation in M&A activity has lifted steadily in recent years, rising from 20% in 2016.

Part of this increase can be attributed to Australia’s reputation as a stable, well-regulated market in a time of global uncertainty and heightened geopolitical tensions.

Foreign investors are paying a significant premium for Australian companies. As a guide, in 2022, the median EV/EBITDA paid by foreign buyers peaked at nearly 14.8x, almost double the 7.44x paid by local buyers, indicating a strong willingness to pay more for strategic assets.

Foreign buyers tend to target larger transactions though. For instance, in 2021 and 2022 the average foreign transaction values spiked over $500 million. By contrast, local deals generally remained below $250 million.

Local against foreign number of transactions in Australian Market with associated proportion

M&A activity by industry

Within the Australian market, M&A activity (by deal count) has remained concentrated in a handful of sectors since 2016.

The Consumer Discretionary sector contributed a meaningful share to the mix, accounting for close to one in ten (9.4%) deals in 2025. Here too though, this represented a decline from 13.4% in 2023.