The term ‘bond vigilantes’ might initially appear as though it could be the name of a rock band. However, the term was coined back in the 1980s and describes investors that sell off government bonds (i.e. push prices down and yields up) when they perceive policies as inflationary or unsustainable. The bond vigilantes crashed US President Trump’s plans around reciprocal tariffs when a huge sell off in US Treasuries after Liberation Day led Trump to press pause for 90 days.

When the US House passed the ‘One, Big, Beautiful Bill (OBBB)’ on 22 May, which extended the 2017 Tax Cuts and Jobs Act, the bond vigilantes intervened once again. US Treasury yields at the long end surged, as fears were flamed about the sustainability of US fiscal policy.

The US Congressional Budget Office estimates this bill will increase the US federal deficit by US$3.8 trillion over the next decade, as the spending increases and tax cuts are not fully offset by expenditure cuts.

Ahead of the House vote on the OBBB, Moody’s downgraded the US sovereign credit rating from AAA to Aa1. It marked the first time since 1917 that the US lost its top credit rating from Moody’s. The credit-ratings agency cited concerns over rising government debt, escalating interest payments and a lack of political will to address fiscal imbalances.

The OBBB is now due to go to the Senate. It’s possible the OBBB does not pass in its current form and there are some revisions. As it stands right now, the additional supply of US Treasuries needed to fund the OBBB places downward pressure on Treasuries (i.e. prices with yields moving inversely); it’s set to lift the size of federal debt to potentially 125% of the economy, as measured by gross domestic product (GDP).

As bond investors have recoiled at the OBBB, US longer-dated bond yields have surged. The US 30-year bond yield pierced the key technical threshold of 5% on 19 May. It also closed the trading session above 5%, making it the first close above this level since late 2023. Moreover, it was just 31 basis points away from the highest closing rate of 5.40%, a rate which was struck during the height of the global financial crisis in June 2007. The US 10-year bond yield has also increased sharply. It rose 34 basis points, from a close of 4.13% on 2 April, Liberation Day, to as high as 4.63% during the trading session on 22 May. It is currently trading at around 4.40%.

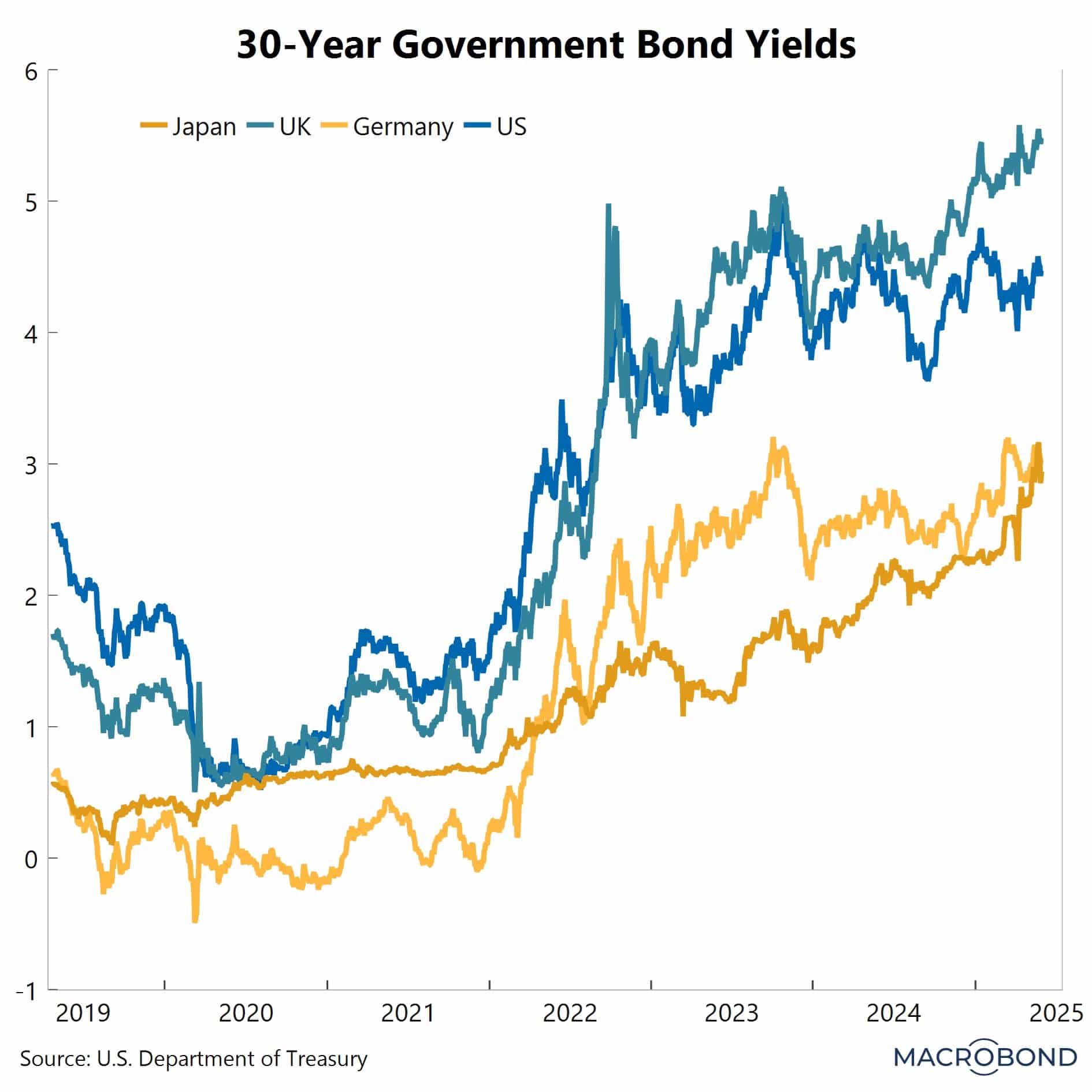

The US Treasury (or bond) market, particularly long-term US Treasury securities, holds a significant influence over global bond markets. This is due to their role as benchmarks for risk-free assets, their impact on global interest rates, and their effect on investor behaviour around the globe. The US bond market is also both the largest and the most liquid in the world.

Therefore, the rise in longer-dated bond yields has not been confined to just the US. In fact, it is a trend that can be observed in other major economies, such as the United Kingdon, Europe (represented by the German Bunds market) and Japan. There are also rising concerns around massive budget deficits in these respective economies. Increases in defence spending is a part of the blowout in deficits, driven by a response to heightened geopolitical tensions. Interestingly, the 2025 Global Risks Report, published by the World Economic Forum, identified state-based armed conflict as the most immediate global risk for the year. This finding was released just five days before Donald Trump’s inauguration on 20 January, which marked a significant shift in US trade policy and has upended the multilateral trading system.

In Australia, the US 10-year yield has tracked the movements in US 10-year yields closely, as demonstrated in the chart below on the right. Higher yields mean higher borrowing costs for consumers, businesses and governments. Central bank policymakers will need to consider these implications in their future rate-setting decisions. In the US, home lending is mostly fixed at 30 years. In Australia, fixed home loan rates account for a modest share of lending and typically are between one and three years. But the impact won’t just rest at housing.

So far, the major share market bourses in the US and the ASX 200 index have held up remarkably well; for example, both indexes are not far off their peaks struck in February. The US share market bellwether, the S&P 500 index, is less than 4% away from an all-time peak and the ASX 200 share market index is 2% away from a record high. Higher long-term interest rates typically weigh on equity valuations, particularly for growth stocks with earnings far in the future. However, equity markets have remained resilient, supported by robust corporate earnings, expectations of further rate cuts and perhaps some rotation of capital from bonds into equities. How long markets can remain at these levels warrants close monitoring.

The information in this article is general in nature, intended for informational purposes only and does not constitute financial, investment, legal or professional advice; readers should seek guidance from qualified professionals before making decisions based on its content.