Today’s inflation data was widely anticipated because it would give us the first read on the spillover of higher fuel prices to the broader economy after the initial oil shock in March. It is fair to say it did not quite live up to the hype, with the results coming in line with market expectations. There will be more hype later today. The Blues and Maroons will take care of that. And if that does not settle it, the World Cup next month will give us something else to get behind.

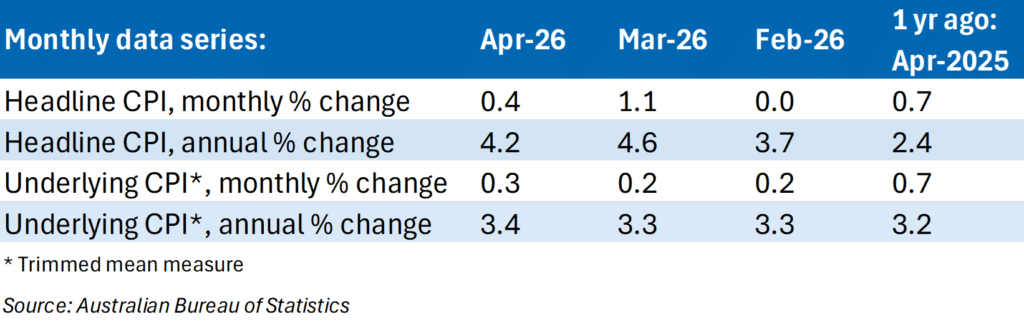

Why didn’t it live up to the hype? The underlying inflation measure, which we are watching more closely, was in line with market expectations. It rose 0.3% in April and the annual rate edged up from 3.3% in March to 3.4% in April. We had seen some risk that spillovers could be stronger, but this did not eventuate in this print.

The headline rate of inflation rose 0.4% in April, taking the annual rate from 4.6% in March to 4.2%. The softening in annual terms was driven by lower auto fuel prices following the government’s decision to cut the fuel excise by 50% from 1 April. However, this is a temporary effect. Since the outbreak of the war, automotive fuel prices are close to 24% higher. The fuel tax relief will not prevent broader spillovers. The risk is that the effects of higher fuel and fertiliser costs, driven by the war, widen and deepen over time, particularly with a peace deal yet to be reached and setbacks never far away.

There is already evidence of this feeding through. The Australian Bureau of Statistics noted that higher oil prices are lifting costs in sectors exposed to freight and logistics, such as parcel delivery and construction. This is reflected in price increases of 12.4% for postal services and 4.7% for new dwelling construction over the past year.

In April, housing remained the largest contributor to inflation, reflecting its weight in the basket. Electricity (+22.5%), new dwellings (+4.7%) and rents (+3.5%) were the main drivers of the annual increase. On a monthly basis, clothing and footwear recorded the strongest growth, rising 3.9%, while the transport group saw the sharpest decline (-2.7%).

The RBA next meets on 15–16 June and we continue to expect it to remain on hold after three consecutive rate rises. The softer labour market data last week, together with today’s inflation print, supports a pause as the Bank assesses the impact of earlier tightening on the economy.

We still see a risk of one more rate rise with the likely timing being in the September quarter. Inflation risks remain tilted to the upside, led by new housing costs as higher diesel, freight and petrochemical prices continue to feed through supply chains. At the same time, the threshold for further tightening has lifted. Sentiment around the Federal Budget tax changes and emerging weakness in the labour market points to the possibility of a faster cooling in economic activity.

In terms of the impact of the rate rises in February and March, there is early evidence that spending on both essentials and non-essentials is easing, although the adjustment is gradual. Consumers are not yet fully acting on the deep pessimism evident in survey data. The gap between sentiment and behaviour remains.

In April, inflation for both essentials and non-essentials softened in annual terms, although essentials inflation remains materially higher. Meanwhile, annual goods and services inflation both eased in April, although each remains above the RBA’s target band.