The sharp rise in US long-end yields has opened divergences in markets. One market is currencies. The spike in US long-term yields has led to a sharp sell-off in the US dollar (USD) index, which represents the US dollar’s value against a basket of major currencies. The sell-off in the USD index reflects investors adjusting their portfolios in response to erratic policymaking around tariffs, as well as the deteriorating US fiscal situation.

The USD sell-off combined with surging long-term Treasury yields represents an unusual divergence, given that rising US bond yields typically strengthen demand for the dollar.

But the factors behind the rise in higher US long-end yields perhaps underscore a possible structural shift underway. US long-end yields are being driven higher by fiscal concerns and the uncertainty and unpredictability of US tariffs policy. It is not being driven by expectations of stronger economic growth. It means investors are demanding a higher premium to shoulder the risk of owning longer-term debt. The term premium is the extra return that investors require for holding long-term bonds instead of repeatedly rolling over shorter-term debt. It has risen to its highest level in a decade (see the chart on the term premium).

Without a meaningful reduction in the US budget deficit, investors may not regain confidence around fiscal sustainability. This could keep the term premium at elevated levels while encouraging investors to continue shifting away from US government Treasuries.

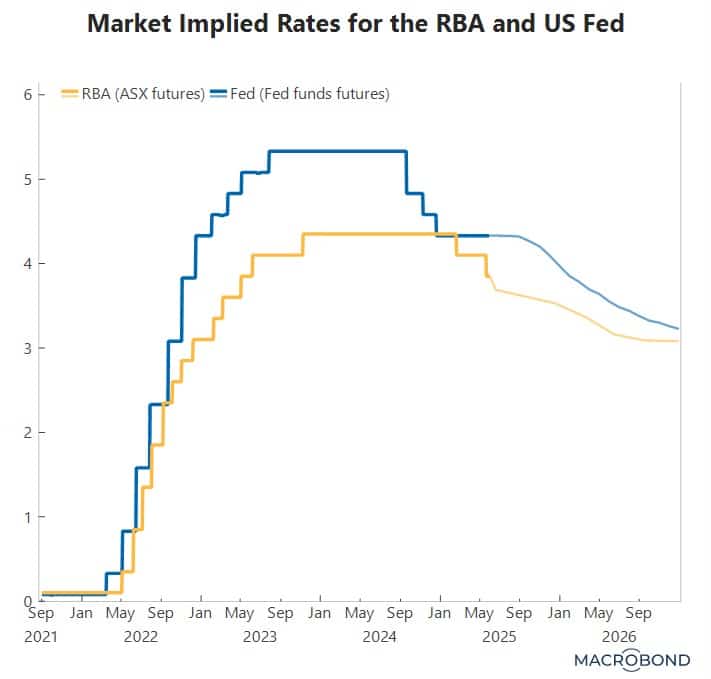

At the same time, tariffs and stimulus from the ‘One, Big, Beautiful Bill (OBBB) are inflationary for the US economy, suggesting the US Federal Reserve may have to hold the Federal funds target rate higher for longer. The US Fed kicked off its easing cycle in September 2024, cutting rates by a cumulative 100 basis points through the second half of the year. However, uncertainty over how tariffs might affect the economic outlook has contributed to policymakers maintaining their pause on further cuts, with monetary policy settings unchanged since December.

On April 2, US President Trump announced reciprocal tariffs on most economies, with rates eventually reaching up to 145% on China—effectively constituting an embargo on Chinese trade. On 9 April , Trump declared a 90-day pause on these tariffs for most countries, though China remained subject to the higher rates. Subsequently, on 12 May, the US and China agreed to a 90-day truce that reduced tariffs from 145% to 30% and China’s retaliatory tariffs from 125% to 10%. However, a baseline universal tariff of 10% on all countries remains in place, alongside ongoing tariff changes at the micro and sectoral levels. For example, on 30 May, US President Trump announced the doubling of steel tariffs to 50%. The erosion of trust and abrupt, frequent policy reversals mean uncertainty will persist, adversely impacting business investment, hiring decisions and broader economic activity.

Minutes of the 6-7 May meeting suggested broad-based consensus in holding the fed funds rate steady and continuing with a cautious approach amid elevated uncertainty. Tariffs were expected to bolster inflation ‘markedly’ this year and push the unemployment rate up. Fed fund futures have two rate cuts fully priced for this year in October and December. Prior to US President Trump’s Liberation Day, there were almost four rate cuts priced in with the first rate cut priced for June.

Last week, the US Court of International Trade found US President Trump did not have the authority to introduce the levies using the emergency economic powers legislation he cited when he imposed sweeping tariffs on countries around the world last month. This suggests perhaps when the pause ends in July, reciprocal tariffs may not resume, however, the path ahead remains highly unpredictable.

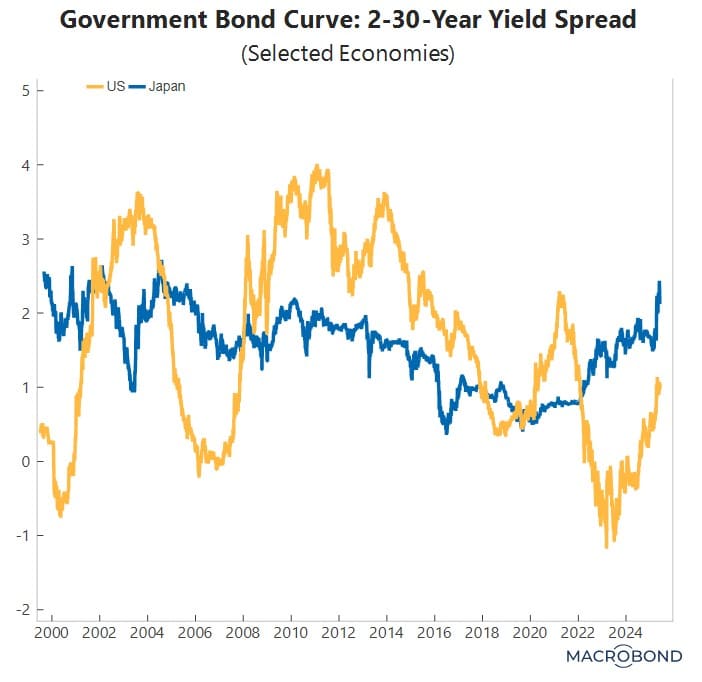

Along with the rise in longer-term yields, there has been a steepening in the yield curve in the major economies, that is, the difference in the 30-year bond yield and the 2-year bond yield has widened. The Japanese government bond curve has experienced the most acute steepening. The Japanese 2-30-year curve has widened to 59 basis points between 2 April and 30 May.

Furthermore, the Japanese 2-30-year spread is wider than the US spread – an unusual occurrence and last sustained for extended periods in episodes of stress, such as during the US recession in the early 2000s, the global financial crisis and covid (see the chart). It could be an amber indicator.

The information in this article is general in nature, intended for informational purposes only and does not constitute financial, investment, legal or professional advice; readers should seek guidance from qualified professionals before making decisions based on its content.