The steepening of the Japanese government bond yield curve is significant and can’t be ignored. The Japanese are a significant net creditor to the rest of the world, especially the US. Unlike in the US, the rise in Japan’s long-end bond yields have more to do with the scaling back of Japan’s bond purchases as inflationary pressures have lifted. Also, Japan’s yield-curve-control (YCC) programme, which operated from September 2016 to March 2024, previously helped anchor Japanese bond yields, but the Bank of Japan (BoJ) ended YCC in March 2024 alongside its exit from negative interest rates.

The era of deflation alongside ultra-low rates in Japan is over, which means the traditional yen carry trade that relied on borrowing in yen to invest in higher-yielding assets elsewhere, such as in US asset classes, is under significant pressure and undergoing a shift.

Recent Japanese auctions of 20-year government bonds and 40-year bonds have drawn weak demand and led authorities at the BoJ and Ministry of Finance (MOF) to start fretting. But the threats in Japan are not the same as those for the US. Importantly, almost all Japanese bonds are domestically held. Japan is also a net creditor nation. These two statements are not true of the US. The US is reliant on foreign capital.

It does not mean we can ignore the rise in Japanese government bond yields because it may redirect Japanese capital away from US Treasuries. There’s some evidence this is underway with the Japanese yen appreciating against the US dollar (see chart below).

Japan’s MOF and BoJ are unlikely to allow a crisis to develop. In a rare move, the MOF last week circulated a questionnaire to primary dealers. This action fuelled speculation that the MOF would step in and support bond prices, by shifting issuance – such as increasing issuances in other parts of the curve and cutting back issuance at the super long end. It could also choose to tweak the shape of its quantitative tightening programme and/or reinvest more from its maturing bonds in the long end of the curve (thus pushing up prices, bringing down yields). The yield on the 30-year Japanese government bond and the super-long 40-year bond have subsequently fallen from their record highs on 22 May.

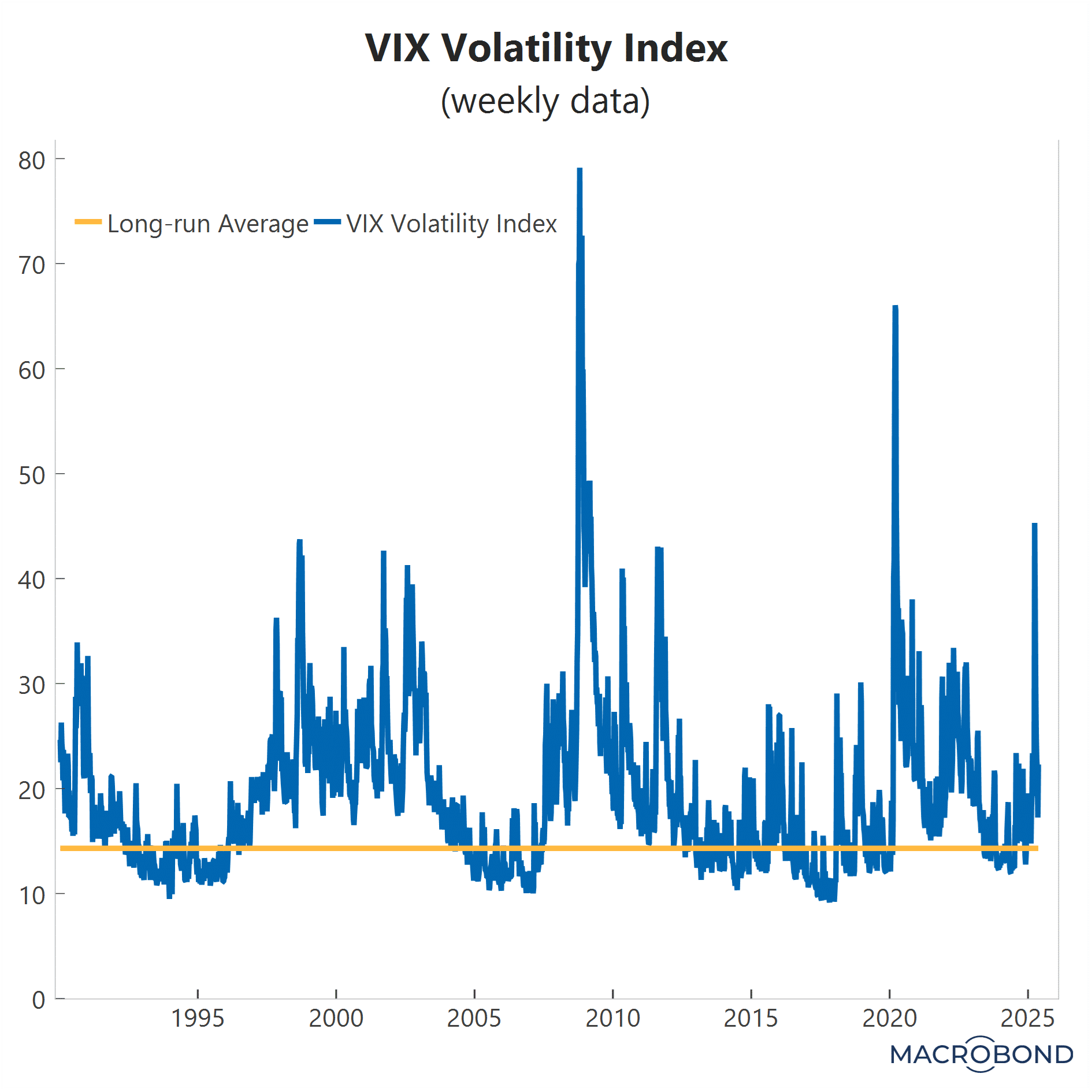

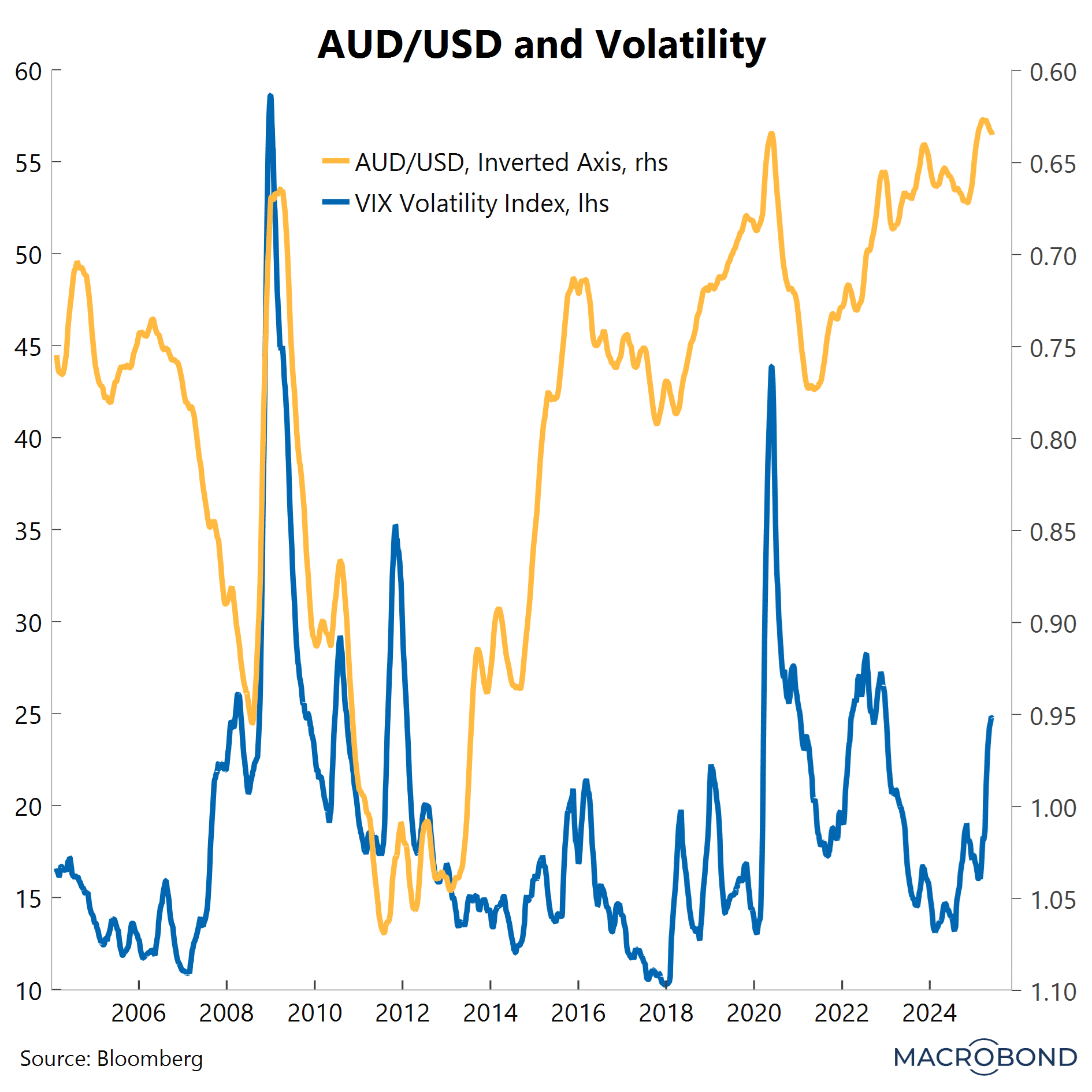

All eyes now turn to the BoJ meeting later this month. The world is watching with bond vigilantes and fiscal deficits back in the spotlight. One thing is certain- rising long-end yields in the major economies and Australia threaten borrowing costs across the board and could add to greater volatility in financial markets, including currency markets. The higher the VIX index, the higher the volatility. The AUD/USD can come under from selling pressures during heightened volatility. In the chart below, spikes in the VIX volatility index have been associated with a weaker AUD/USD (noting the right axis is inverted). However, the concerns about fiscal sustainability in the US that have driven longer-dated US Treasury yields higher could maintain downward pressure on the USD index and limit any sell off in the AUD/USD exchange rate.

The information in this article is general in nature, intended for informational purposes only and does not constitute financial, investment, legal or professional advice; readers should seek guidance from qualified professionals before making decisions based on its content.