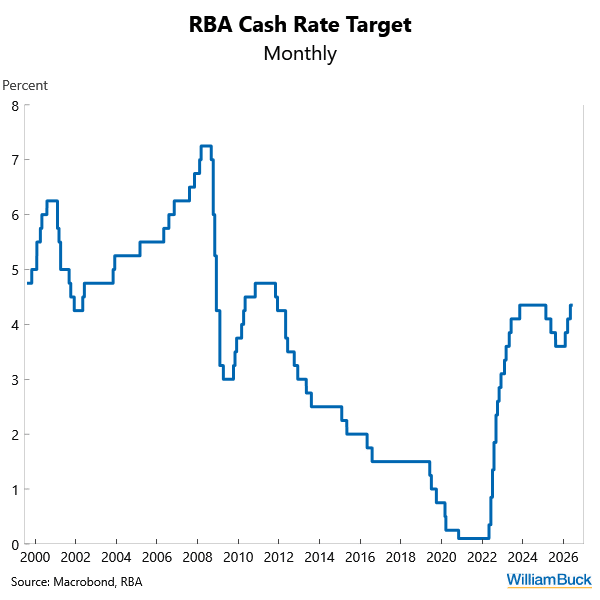

The Reserve Bank left the cash rate unchanged today at 4.35%. After three consecutive hikes, a pause was the sensible step to assess incoming data and gauge how earlier tightening is flowing through to economic activity.

Markets, including ourselves, did not expect a move. This meeting was always less about the decision and more about the tone of the statement and press conference.

At 4.35%, the cash rate is at a restrictive level and sits at the peak reached in the previous cycle. Monetary policy works with lags, and recent increases are still filtering through the economy. The RBA acknowledged this shift in conditions, noting that financial conditions have tightened and there are signs of slowing momentum. At the same time, it reinforced that inflation remains too high.

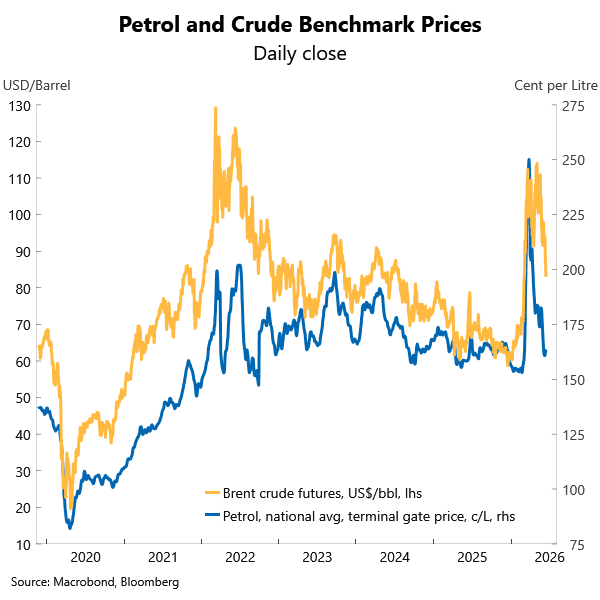

We expect the RBA to maintain a firm tone while inflation sits above target. However, the case for further tightening is weakening. The labour market is easing, housing activity is softening, and lower oil prices are helping to ease cost pressures. The April inflation data also pointed to only modest pass through from earlier increases in oil and urea prices.

A key signal came from the change in language around inflation expectations, which the RBA monitors closely. At the previous meeting, the Bank noted that expectations had risen. Today, this was updated to say that expectations have eased, although they remain higher than earlier in the year. This shift suggests that upside risks are no longer intensifying. With geopolitical tensions easing, there is scope for further moderation.

Looking ahead, inflation is likely to remain elevated in the near term, but the broader trend should begin to soften as demand slows further. While there remains a risk of another rate rise later this year, the hurdle is now higher.

Our forecasts continue to point to rate cuts from around the middle of next year. We retain this view, although recent experiences tell us a year is a long time in economics! Economic uncertainty has not vanished and remains elevated.