International equities

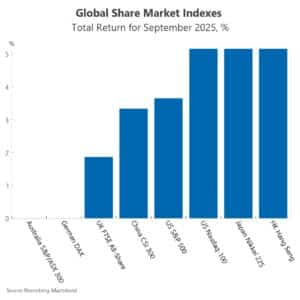

Global share markets delivered strong gains in September with the benchmark Morgan Stanley Capital International (MSCI) World Index rising 3.1%. US equities led the way as the US Federal Reserve cut the federal funds rate by 25 basis points on 17 September, marking its first reduction of the year. The Nasdaq and S&P 500 indexes both recorded multiple record highs during the month, delivering total returns of 5.5% and 3.6%, respectively. The accompanying dot plot published by the Fed suggested two further rate cuts before year’s end, although views among policymakers were notably divergent. While sticky inflation and weakening jobs data caused intra-month volatility, equities remained well supported by expectations of additional rate cuts and strong earnings results. Interest-rate markets are currently anticipating four more Fed cuts by the end of 2026.

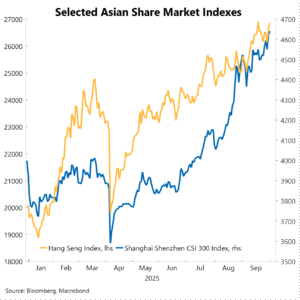

Asian markets were the standout performers. Hong Kong’s Hang Seng index jumped 7.6% in September, while China’s CSI 300 index rose 3.3%. Chinese equities have been particularly strong over the past six months, surging 21.9% with tech stocks leading the rally. This performance has been underpinned by government policy support for domestic chipmakers, China’s anti-involution policy to reduce cutthroat competition, rising investment in AI and an easing in US-China trade tensions. China’s rally has defied the broader state of the Chinese economy. The sharp gains in China and Hong Kong’s share market helped drive a 7.0% return in emerging markets in September, more than double the 3.1% return in developed markets. Japan’s TOPIX index also delivered strong gains, supported by a favourable US-Japan trade deal that reduced tariffs on most Japanese exports to the US from 25% to 15%. The ongoing refocus on shareholder returns across corporate Japan has also continued to attract buyers to the Japanese equity market.

European markets lagged its US and Asian counterparts. Germany’s DAX shed 0.1% in September while the UK’s FTSE index rose 1.9%. Both the European Central Bank and Bank of England met in September and left policy rates unchanged. Unlike the US, both central banks appear to be at or near the end of their easing cycles. The French CAC 40 index delivered a firm return in September, despite political instability. After a vote of no confidence, France’s former Prime Minster Bayrou was replaced with the current Prime Minister Lecornu.

From a style perspective, growth stocks significantly outperformed value stocks during the month. Large technology stocks continued to benefit from strong demand for AI-related equities, with the ‘Magnificent 7’ tech giants jumping 9.0% in September alone.

Australian equities

The Australian share market underperformed international peers in September 2025. The S&P/ASX 300 index returned a loss of 0.7% during the month, following a solid return of 3.2% in August. After reaching a record high of 8,954 on 21 August, the Australian market struggled to establish a new high in September. This is in stark contrast to international markets, such as the US S&P 500, where fresh record highs during the month occurred frequently.

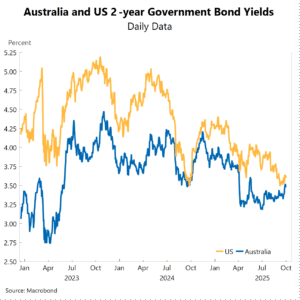

|

|

Domestic data releases throughout September provided a mixed backdrop for Australian equities. Early in the month, data revealed an economic recovery proceeding faster than anticipated by both markets and the RBA. Gross domestic product (GDP) increased by 0.6% in the June quarter and by 1.8% in the year to the June quarter 2025, exceeding consensus forecasts of 0.5% and 1.6%, respectively. This stronger recovery was driven primarily by consumer spending growth.

The jobs report mid-month showed employment fell in August, suggesting the labour market was losing some momentum. However, the unemployment remained low at 4.2%.

Market sentiment around future rate cuts shifted dramatically later in the month when the monthly inflation gauge revealed potential upside risk to inflation. The RBA’s preferred measure remains the quarterly inflation data, next due in late October. However, this monthly data sparked market concerns that the RBA might delay rate cuts longer than anticipated. This pressured rate-sensitive sectors and prompted markets to significantly reduce expectations for near-term rate cuts and the overall easing cycle.

At the RBA’s 30 September board meeting, they left the cash rate unchanged at 3.60% as widely expected, but the statement and Governor’s remarks reinforced the market’s more cautious rate-cut expectations.

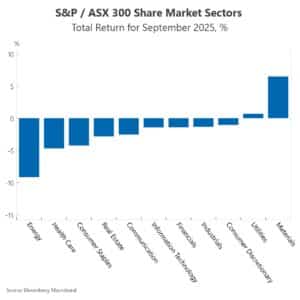

Market pricing around the possibility that the RBA may delay easing and may not have much scope for further cuts contributed to a sell-off across most sectors during the month. Only materials and utilities recorded gains among the eleven share market sectors.

Materials was the best-performing sector, rising 6.5% in September. The stocks of gold producers drove this increase, with gold reaching a fresh all-time high of US$3,859 per troy ounce on 30 September, an 11.9% jump for the month and a whopping 47.0% increase year to date. Mining giants, BHP and Rio Tinto, recovered from losses early in September after a significant mine outage at Freeport-McMoRan’s Indonesian operation raised concerns over a potential copper deficit.

Energy was the worst-performing sector, falling 9.1% in September. The sector was weighed down by the collapse of Abu Dhabi National Oil Company’s high-profile takeover bid for Santos on 17 September. The deal fell apart amid concerns around valuations, capital-gains-tax allocations, regulatory approvals, a methane leak disclosure issue and escalating potential costs. Santos’s share price shed nearly 14.0% during the month. Its setback pressured most other oil and gas equities. Softer world oil prices, driven by the Organisation of Petroleum Exporting Countries’ (OPEC) efforts to lift supply, also provided little support to the sector.

Investors also continued to shy away from selected stocks that performed poorly in the most recent profit reporting season, including big names such as Woolworths and CSL, down 7.3% and 6.9%, respectively. Both stocks extended the losses recorded in August. The rotation away from the Commonwealth Bank (CBA) also continued. The share price of CBA dropped 2.0% in September and is now down 14.7% from its closing peak of $191.40 struck on 25 June. Westpac and National Australia Bank rose through September, but ANZ pulled back.

Fixed income and currencies

Expectations around monetary policy, geopolitics and concerns around US fiscal sustainability delivered volatility for global bond markets in September. The global fixed interest fund returned 0.7% in September, supported by stronger US Treasury prices. The yield on generic US 2-year and 10-year Treasuries, fell 1 basis point and 8 basis points, respectively in September.

The rally in US government bonds was driven by a shift in market focus from upside inflation risks to downside risks around the economic growth outlook. The US Federal Reserve’s preferred measure of inflation remains sticky and above the inflation target, but the rapid cooling in the labour market has led markets to focus more on the growth outlook. In the three months to August, non-farm payrolls have averaged just 29,000, a marked slowdown from the prior three-month period and from the start of the year when the three-month average was 232,000. The US Bureau of Labour Statistics also revised payroll employment growth lower by a much larger than expected 911,000 jobs in the 12 months to March 2025, suggesting the US economy is not as robust as previously thought.

Markets are currently pricing in four more rate cuts from the US Federal Reserve before the end of next year with almost two cuts fully priced before year’s end in 2025.

In key European bond markets, the government yield curve also flattened, as shorter-dated yields rose and longer-dated yields stayed elevated. Renewed attention on the UK’s fragile fiscal situation ahead of the November budget helped push the 30-year Gilt to 5.69% in early September – its highest level since May 1998.

Japan’s bond market was impacted by both political and fiscal uncertainty following Prime Minister Ishiba’s resignation on 7 September. Japan’s 30-year yield rose to a record close of 3.29% on 3 September and the 10-year government bond yield rose to 1.65% on 22 September – its highest since the global financial crisis. Persistent inflation remains a concern. Whilst the Bank of Japan held policy steady at its September meeting, markets are pricing in a 25-basis-point rate hike by March 2026, with another rate hike to follow before the end of 2026.

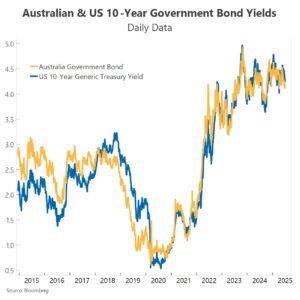

Turning to domestic trends, Australian government bonds sold off in September with the Australian 2-year yield rising 15 basis points over the month and the 10-year rising 2 basis points. The rise in the shorter-end yields reflects the market repricing around future rate cuts. The modest gain in the Australian long end reflected developments in US bond markets.

In credit markets, a weaker US dollar provided a tailwind for emerging market debt. Spreads tightened across both high yield and investment grade bonds in the US, suggesting US bond markets are still not seeing much default risk across the corporate bond market. The US dollar index softened 0.6% in September, falling to a low of 96.22 on 17 September – its lowest level since 23 February 2022. The low was recorded amid market expectations that there was some risk the Fed could cut by as much as 50 basis points at its meeting on 16-17 September.

The Australian dollar appreciated 1.5% against the US dollar in September, reaching its highest level in 11 months on 17 September, at 0.6707. The AUD/USD failed to push higher after weak domestic jobs data pushed it off this high. In trade-weighted terms, the Australian dollar strengthened 1.4% in September.

Property and infrastructure

The Australian listed property sector returned a loss of 2.9% in September, following a period of strong growth. Indeed, over the past six months, Australian listed property has delivered a total return of 18.8%. Goodman Group led the sector lower in September with a 4.6% decline in its share price. Despite the broader support for data centres globally, Goodman has now declined 10.8% year to date, as investors have become concerned over the lofty valuations the stock has reached.

Globally, listed property returned a loss of 0.4% in September and listed infrastructure rose 0.4%.

Economic outlook

The US Federal Reserve’s recent rate cuts have strengthened demand for equities. Investor confidence remains buoyant, liquidity is abundant and the structural transformation driven by AI continues to fuel enthusiasm for technology stocks. However, valuations have climbed to elevated levels, with September bringing increased discussion about potential AI-related bubbles.

The Fed’s decision to resume cutting rates was primarily motivated by labour market concerns. Historically, weakening employment growth signals emerging pressure on corporate profitability. Significantly, the Fed began easing even as its preferred inflation measure—the core personal consumption expenditure deflator—runs at nearly 3% annually, well above target. This raises stagflation risks in the U.S., while ongoing trade tariff uncertainty further obscures the economic outlook.

Against this backdrop of heightened uncertainty, equity markets have shown remarkable resilience. When a US government shutdown loomed in late September, markets dismissed the threat entirely. This suggests investors may be overweighting positive developments while insufficiently discounting genuine risks.

While further Fed rate cuts should support equities, the elevated uncertainty underscores the importance of diversification across both asset classes and regions. Gold has reached new record highs and may climb further, offering a valuable hedge against potential upside inflation risks. Markets currently anticipate four additional US rate cuts totalling 100 basis points by end-2026.

Australia presents more favourable fundamentals. Underlying inflation sits within the RBA’s 2-3% target band, unemployment remains low despite some moderation in job creation, and economic recovery appears more firmly established. We expect two additional RBA rate cuts before mid next year, which should provide further support for Australian equities. While markets are pricing in just one additional cut, we believe the labour market has more slack than the RBA currently estimates and that the household spending recovery, though underway, has been overstated.

Disclaimer

This report has been prepared for general informational purposes only and does not constitute personal financial advice. It does not take into account your specific objectives, financial situation, or needs. Before acting on any information in this report, you should consider its appropriateness in light of your circumstances and seek independent financial advice. No representation or warranty is made as to the accuracy, completeness, or reliability of the information contained herein. Past performance is not a reliable indicator of future performance.