The jobs market has continued to soften, as we have previously warned in our research, and continues to leave the door open for a November rate cut. While our conviction around a November rate cut weakened after the last RBA meeting, we maintained our forecast, primarily based on our expectations for the jobs market.

Today’s data confirms our expectations for the employment market. The unemployment rate rose to a near 4-year high of 4.5% in September, up from an upwardly revised 4.3% rate in August (previously reported as 4.2%). This result was higher than consensus forecasts of 4.3% and exceeds the RBA forecast for the December quarter of 2025 of 4.3%. While today’s data is for September, it suggests the starting point is higher.

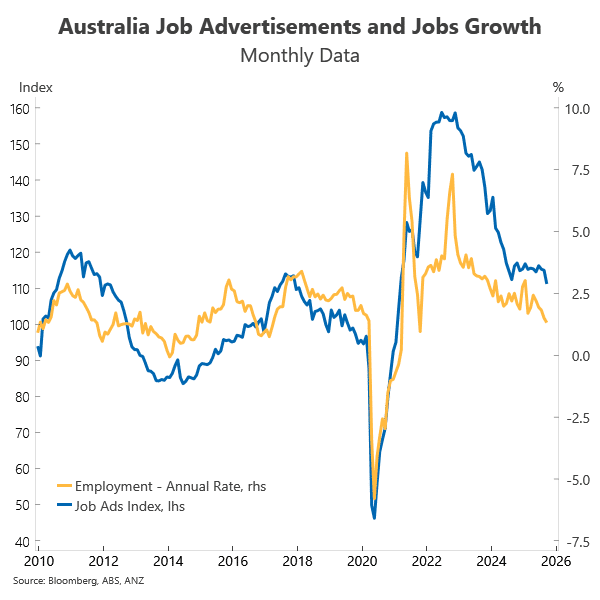

Job vacancies data, which is a leading indicator of jobs growth, has also been weakening, and recruiter liaison is consistent with this weakening in employment growth. The most recent jobs advertisements data published by ANZ and Indeed showed a 3.3% drop in September – the largest decline since February 2024 and the third consecutive fall.

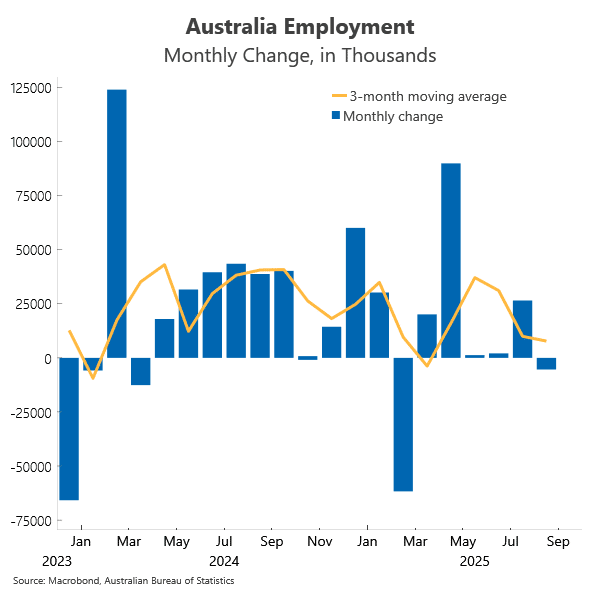

Employment rose by 14,900 jobs in September, with nearly 9,000 jobs being full-time. A slight tick higher in the participation rate (66.9% to 67.0%), reflecting more people actively looking for work, has contributed to the rise in the unemployment rate. But even if the participation rate had stayed steady, the unemployment rate would have risen.

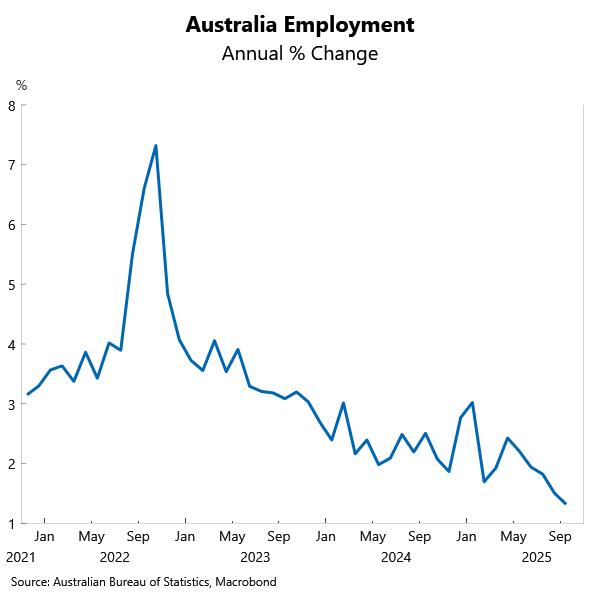

Whichever way we cut the data, there’s a clear slowing underway. Employment growth was 1.3% in the 12 months to September, the softest result since March 2021. Moreover, in the 12 months to September, a net total of 190,500 jobs were created, well down from the 426,800 recorded just nine months earlier in January.

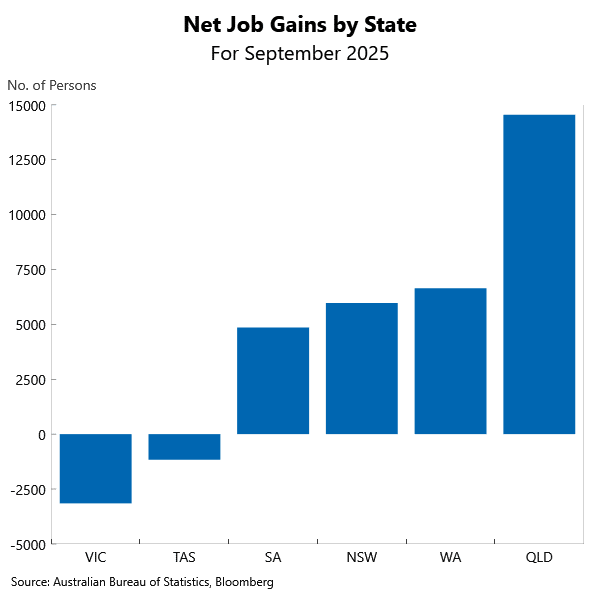

Across the states, the picture was mixed, but in recent months employment growth has been notably soft in New South Wales, where employment growth has slowed to 0.1% in the year to September – the weakest result since October 2021. In September alone, the strongest jobs gain was in Queensland with 4,500 jobs, and the weakest was a loss of 3,200 jobs in Victoria.

Financial markets had a 39% probability attached to a rate cut next month just before the release of today’s data. That probability has risen to 69% and had been more than 100% (i.e., fully priced in) in the immediate wake of the data’s publication.

This is one shoe down with another to come – with the quarterly inflation data due on 29 October. The RBA is concerned that there are components in the monthly inflation gauge that point to upside risks in the quarterly result. We are forecasting a rise of 0.8% in the quarter for an annual increase of 2.7% in underlying inflation, which would make November a close call. A result of 2.8% or higher could delay the next rate cut. Renewed tensions between our largest trading partner, China, and the US also add to the case for the RBA to cut again before the end of the year.

RBA Governor Bullock’s description of monetary policy as “marginally tight” at a Washington forum reinforces our view that further easing is ahead. We maintain our forecast for two more rate cuts before mid-next year, with the next cut in November.

The information in this article is general in nature, intended for informational purposes only and does not constitute financial, investment, legal or professional advice; readers should seek guidance from qualified professionals before making decisions based on its content.