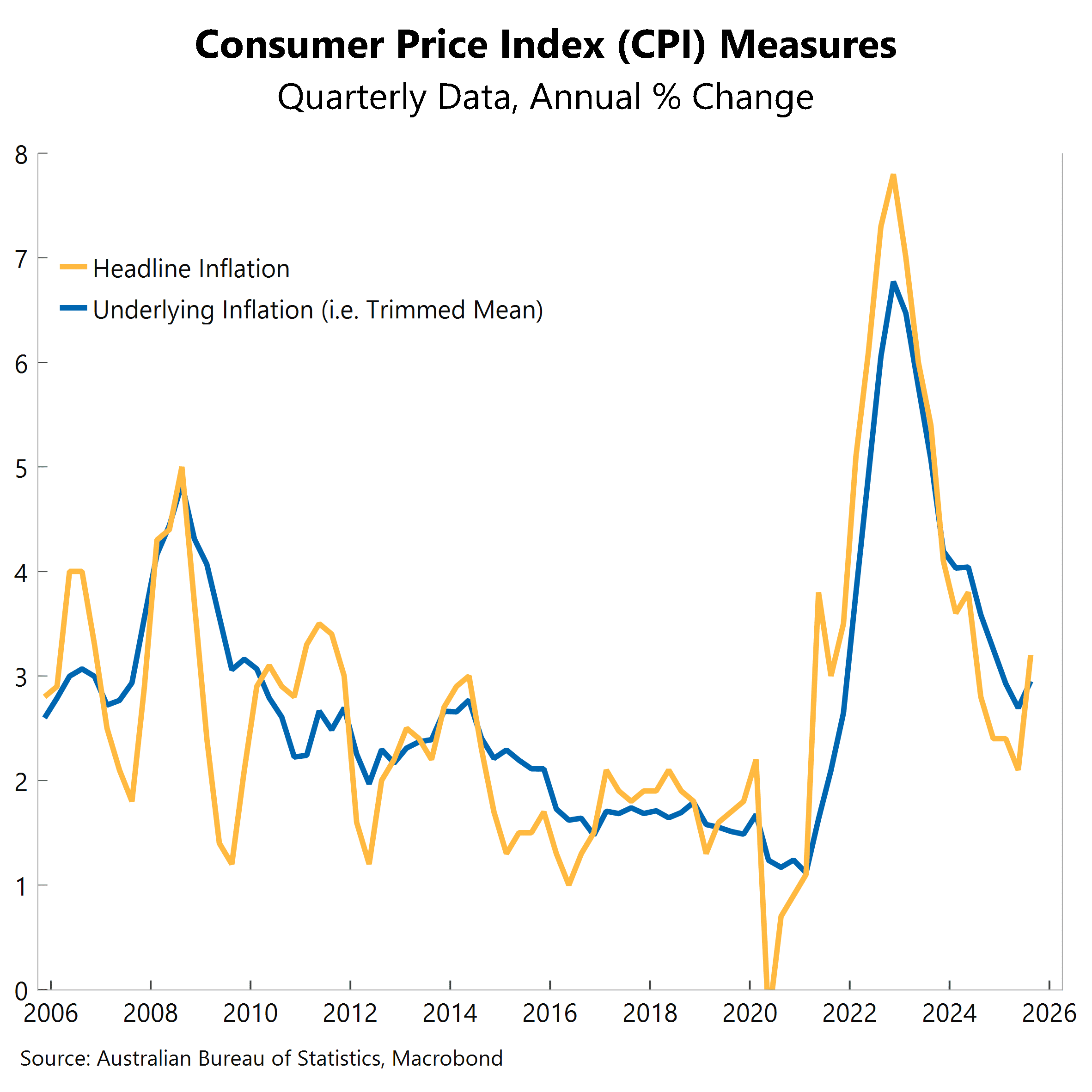

Underlying inflation, as measured by the trimmed mean – the RBA’s preferred gauge – surged past expectations in the September quarter, taking a November rate cut firmly off the table. The quarterly increase of 1.0% significantly exceeded both our forecast and the consensus among economists, which had centred on 0.8%.

The annual rate of underlying inflation accelerated from 2.7% in the June quarter to 3.0% in the September quarter, marking the first increase in the annual rate since its peak in late 2022. This uptick signals that the return to the midpoint of the RBA’s target band will take longer than previously anticipated. The result also sits at the top of the inflation target band and above the RBA’s implied forecast of approximately 2.7% per annum for the September quarter.

Following the RBA board meeting in September, we noted that our November rate-cut call had become less certain and would hinge critically on incoming employment and inflation data. Today’s release settles that question.

The jobs data showed a further loss of momentum, initially suggesting a November rate cut remained possible. However, Governor Michele Bullock threw cold water on that prospect in a fireside chat with the Australian Business Economists on Monday night. She leaned heavily on upside inflation risks and dismissed the rising unemployment rate, noting it remains “pretty low” with jobs “still being created, just not as many.” Her comments set a high bar for today’s inflation print.

We estimated a quarterly result of 0.6% or lower would be needed to trigger a November cut, with even 0.7% borderline. The actual result of 1.0% blew past these thresholds. A Bloomberg poll of 24 economists showed forecasts ranging from 0.7% to 1.0%. Only two predicted the top of that range.

We still expect the Reserve Bank to cut again. Monetary policy remains a little restrictive. However, the timeline has shifted dramatically. We had expected two more rate cuts in November and February, but now forecast only one more cut in this cycle and not before Q2 2026.

The RBA will need to see at least two more quarterly inflation reports before moving. If the December quarter result for underlying inflation (published in January) exceeds 0.6%, the annual rate would breach the top of the target band. That’s a demanding threshold; 0.6% represents the lowest quarterly growth rate in three years and has been achieved only once.

With the economic recovery gaining traction and inflation proving sticker, there’s a genuine risk the easing cycle has already ended. Our base case for one final cut hinges on global growth risks and further labour market softening.

Other central banks have cut rates with inflation above target when labour markets weakened decisively. While we expect Australia’s jobs market to cool further, the bar for RBA action has risen substantially.

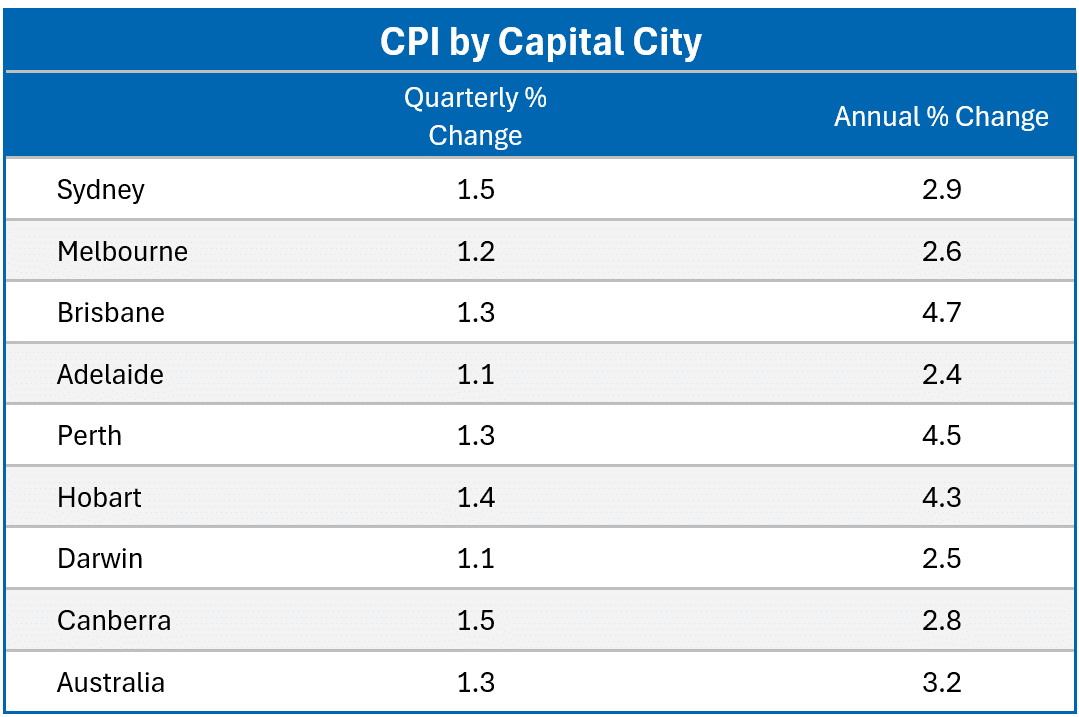

The headline inflation rate rose 1.3% in the quarter and 3.2% in the year. Gains were solid in both goods and services inflation, each rising by 1.3% in the September quarter.

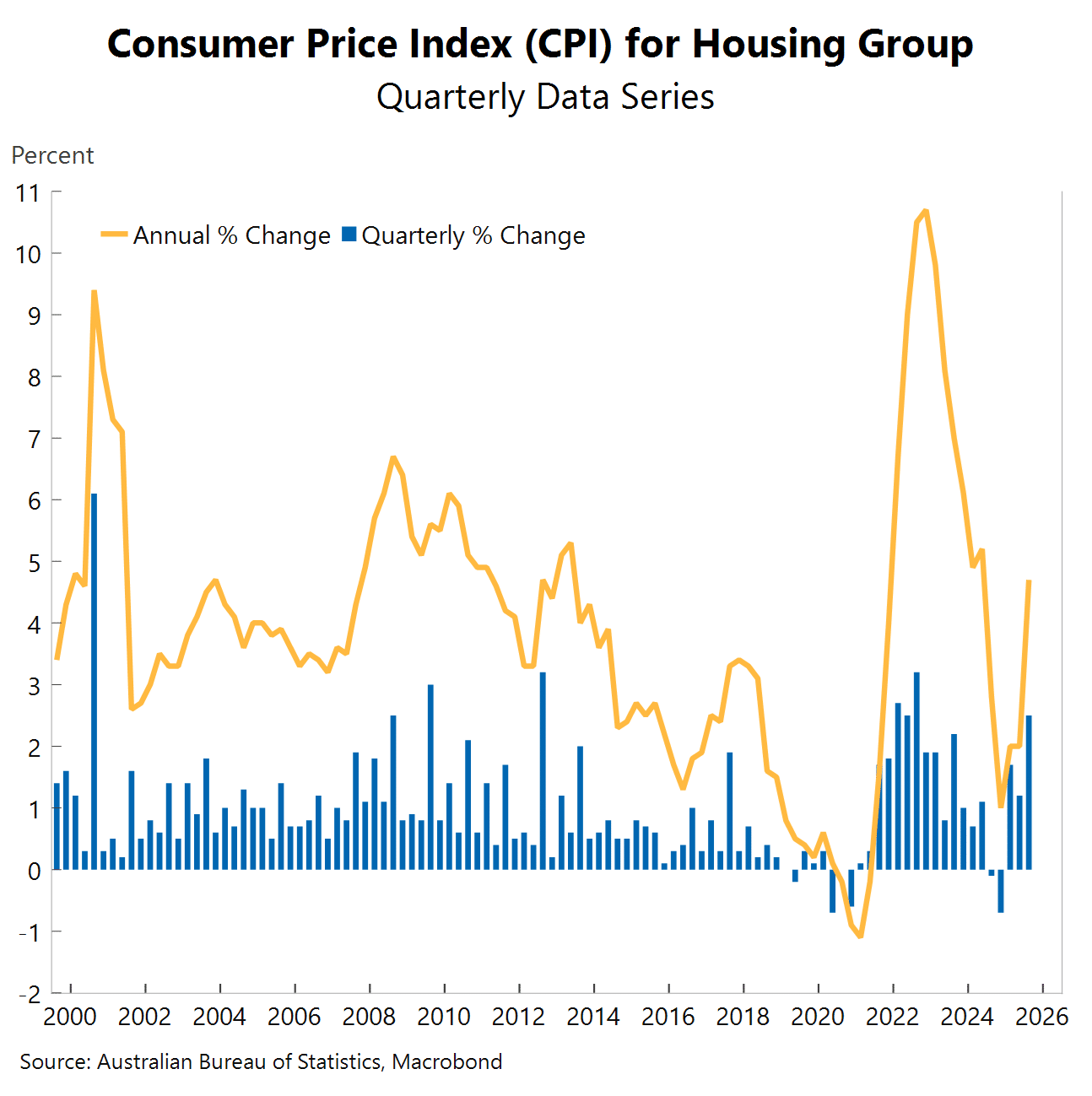

The group that recorded the biggest increase was housing, which rose by 2.5% in the quarter – the largest gain in three years, driven by strong increases in electricity (+9.0%), utilities (+7.1%), gas and other household fuels (+6.7%) and property and charges (+6.3%). In the year to the September quarter, housing inflation lifted by 4.7%, the fastest in nearly three years.

Across the 11 groups, five grew faster than 3%, the upper part of the RBA’s target band, compared with four in the June quarter. In addition to housing, these include alcohol & tobacco, health, education and food.

In terms of all goods and services, 39.1% saw growth exceeding 3%, up from 36.8% in the June quarter, and up from the recent trough of 35.6% in the March quarter.

Across the eight capital cities, three have headline inflation growing at an annual rate above 3% – Brisbane (+4.7%), Perth (+4.5%) and Hobart (+4.3%) compared with none in the June quarter.