Inflation data released today underscores the inflationary impact of the hostilities in the Middle East on Australia. Importantly, inflation was already running uncomfortably high and above the inflation target band before the conflict in Iran began. The escalation has since compounded the challenge facing the RBA.

The release included the quarterly inflation series, still the RBA’s preferred measure, alongside the newer monthly indicator. Across both series, and for both headline and underlying measures, the trend was not our friend. Inflation either stepped up or remained elevated.

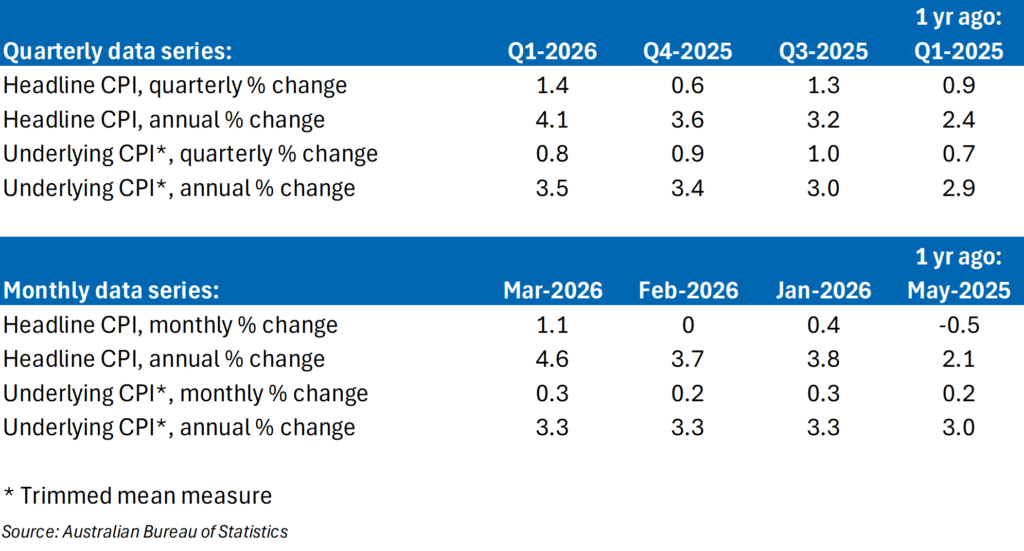

Headline inflation rose by 1.4% in the March quarter, the largest quarterly increase in three years, lifting the annual rate from 3.6% in the December quarter of last year to a 2½-year high of 4.1%. This also marks the third consecutive quarterly increase in annual headline inflation.

The monthly series painted an even more concerning picture, with prices rising 1.1% in March, the biggest monthly increase in eight months, and pushing the annual rate up from 3.7% to a series high of 4.6%.

Much of the acceleration in May reflects the impact of the closure of the Strait of Hormuz on fuel prices in Australia. While the intensity of the conflict has eased somewhat with a ceasefire holding for now, a peace deal has proven elusive. The ongoing closure of the strait continues to disrupt around 20% of global oil supply and roughly one‑third of global fertiliser exports, keeping pressure on energy and input costs.

Unsurprisingly, automotive fuel prices surged in March, rising 32.8% and contributing 1.0 percentage point to the monthly increase in headline inflation alone. This was the sharpest increase on record, albeit in a relatively short data series that begins in 2017. The government’s temporary three‑month reduction in the fuel excise will help constrain fuel’s contribution to April inflation, though only partially.

Higher fuel costs flowed through quickly to broader price measures. Tradables inflation lifted sharply, from 1.3% in the year to February to 4.4% in the year to March, despite the support of a stronger Australian dollar. Goods inflation showed a similar sharp increase, of 3.6% year-on-year to 5.4% year-on-year, highlighting the speed with which global shocks are passing through to domestic prices.

The RBA places greater weight on underlying inflation measures, which strip out the most volatile price movements. While these measures showed a more muted response in the March quarter and the month of March, they nonetheless edged higher. More importantly, they are likely to accelerate in coming months as they begin to capture second‑ and third‑round effects from higher input and transport costs working their way through supply chains and prices. We expect underlying annual inflation to rise to 4.0% in the June quarter, and there is a growing risk it breaches that level.

Business liaison is already pointing to rising input costs and the introduction of fuel‑related surcharges, with firms facing difficult choices. That is, pass costs on to consumers, absorb them through lower margins or deploy some combination of both. Either way, cost pressures are intensifying, demand is likely to soften and the RBA faces a complex calibration challenge.

Domestic inflation pressures remain part of the picture. Market services inflation, which is closely tied to wages and local cost conditions, continues to signal persistent home‑grown price pressure. The RBA’s preferred measure of market services inflation was unchanged at 0.3% in March and the annual rate ticked up to 3.7%.

Against this backdrop, we continue to expect two further rate hikes from the RBA this year, though the outlook remains highly conditional on the duration and evolution of the conflict.

The RBA meets next week. We see a high probability of another rate increase, which would mark a third consecutive hike in this cycle, taking the cash rate to 4.35%. There is a small chance the RBA Board instead presses the pause button, reflecting the lack of unanimity at the last meeting and the lags in monetary policy transmission. However, with inflation both elevated and rising, if May proves to be a hold, June is almost a sure bet.

We also expect another hike in the September quarter, taking the cash rate to 4.60%, which we see as the peak for this cycle. Swap markets are fully pricing a 25-basis-point increase by June, another in September, and assign around a 70% probability of an additional hike in February 2027.